Discretionary vs Advisory Wealth Management UK: Which is Best?

Choosing between discretionary and advisory wealth management comes down to three things: how much control you want, how fast you need decisions made, and what you’ll actually pay all-in. Choosing wrong can lead to a service that either overwhelms you with approvals or excludes you from decisions you wanted to make.

Both services are regulated by the Financial Conduct Authority (FCA) under the Financial Services and Markets Act (FSMA). Both offer Financial Services Compensation Scheme (FSCS) protection up to £85,000 per person per firm for eligible investment claims. And both will charge you somewhere between 0.75%–1.5% of Assets Under Management (AUM) per year before adding platform and fund costs. The difference is in who makes the decision and when.

Quick Answer: Which Service Is Right for You?

| If you want… | Choose… |

|---|---|

| Speed and hands-off management | Discretionary |

| Final say on every portfolio change | Advisory |

| A professional to act fast during market drops | Discretionary |

| To stay involved and learn as you go | Advisory |

| Help managing complex tax, pensions, and multiple accounts | Discretionary |

| Guidance with a simpler financial plan | Advisory |

| Protection from your own emotional decisions | Discretionary |

| To build confidence over time with support | Advisory |

Side-by-Side: Discretionary vs Advisory Wealth Management UK

| Criteria | Advisory | Discretionary |

|---|---|---|

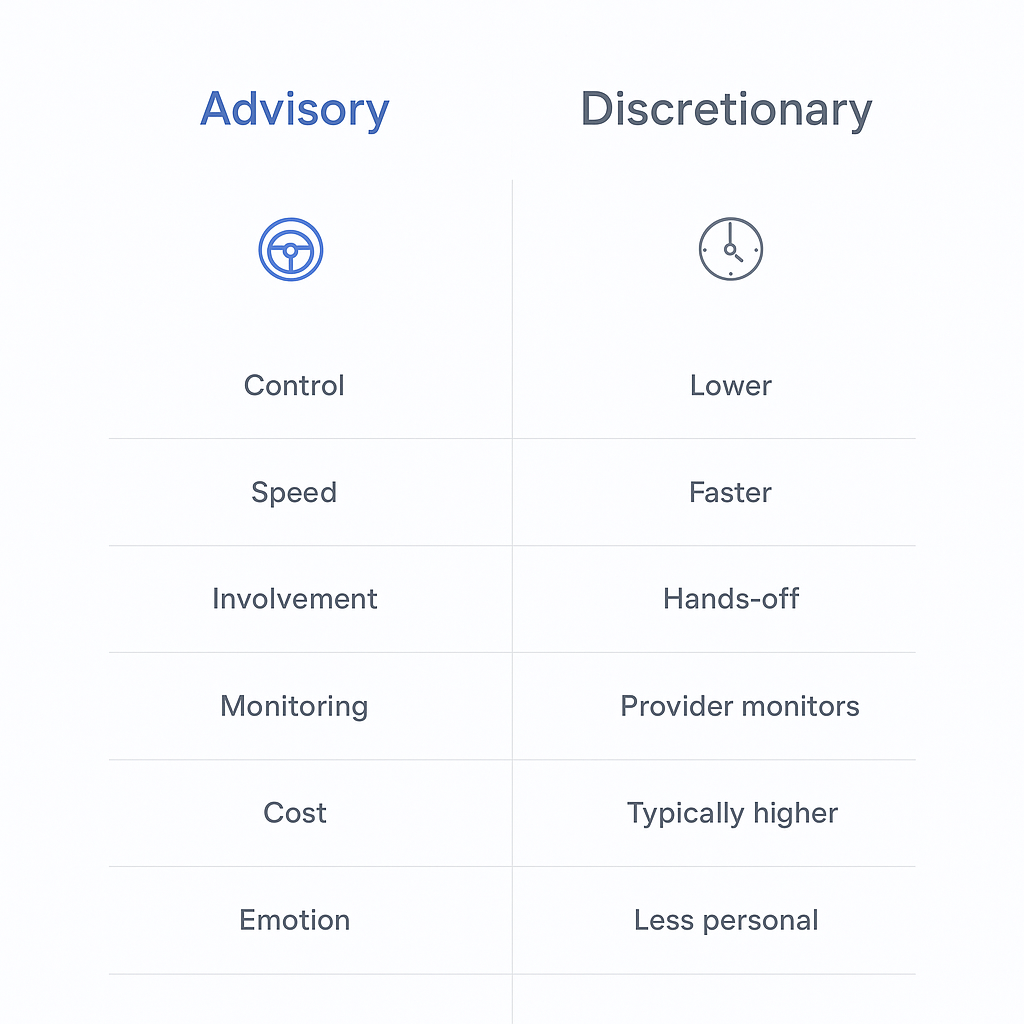

| Control over decisions | Client approves every change | Manager decides within agreed limits |

| Speed of trading | Delayed (needs client approval) | Immediate (manager acts within mandate) |

| Daily involvement | High (you review and respond) | Low (you set the strategy, then step back) |

| Monitoring frequency | Periodic (quarterly/annual reviews) | Continuous, active oversight |

| Typical client fit | Hands-on, financially engaged investors | Busy clients, high net worth individuals, complex portfolios |

| Cost structure (all-in) | 0.75%–1.5% AUM or £1,000–£5,000 fixed + platform/fund add-ons | 0.75%–1.5% AUM (sometimes higher) + platform/fund add-ons; total can reach 2.2% |

| Risk of emotional decisions | Higher (client in the loop during volatility) | Lower (manager acts within pre-agreed risk limits) |

| Transparency/reporting | Proposal documents, approval emails, review meetings | Regular reports and online access after changes are made |

| Range of investments | Can be narrower; some advisors outsource to Discretionary Fund Managers (DFMs) | Often broader; direct market access common |

| Best for | Investors who want control and involvement | Investors who want delegation and fast execution |

| Watch-outs | Approval delays can cost you in fast markets | You give up control; outcomes depend on manager skill |

What “Advisory” Means in Plain English

Your advisor makes recommendations based on your goals, risk attitude, and personal circumstances. Before anything changes in your portfolio, you say yes or no. Nothing moves without your express permission.

Real-life example: your advisor suggests switching from one fund to another. They send you a proposal, explain the reasoning, and wait for your approval. You review it, agree, and then the trade happens. If you say no, nothing changes.

Three ways you’ll notice this in real life:

- Emails or calls asking you to approve a recommendation before action is taken

- Scheduled review meetings (quarterly or annual) where changes are discussed

- Written proposal documents outlining what’s being suggested and why

Advisory works when you have the time and interest to engage. But if markets move fast and you’re unavailable to approve a change, the opportunity or the exit can pass.

Client Communication and Recommendation Approval for Advisory

Advisors present recommendations to clients through methods like email, text, phone calls, video calls, or secure client portals.

Client Approval Process:

Clients review the recommendation and provide approval either electronically (e-signatures are common for security and compliance) or in writing during a meeting.

Response Times:

- Ideally, an immediate acknowledgement (within 10 minutes) is preferred.

- A standard response time is typically within 24 hours or one business day.

Handling Client Unavailability:

If a client is unavailable, firms often use structured processes to ensure knowledge transfer to backup staff (e.g., relationship managers or support teams). This helps maintain service levels.

Follow-Up:

After a recommendation or communication, it is standard practice to send recap notes, outline next steps, and request feedback from the client.

What “Discretionary” Means in Plain English

With discretionary management, you and your manager agree the strategy and risk boundaries upfront. That agreement is called a mandate. After that, the manager can buy and sell within those boundaries without asking you each time.

Real-life example: markets drop sharply on a Wednesday morning. Your discretionary manager rebalances your portfolio the same day, buying what’s underweight, trimming what’s overweight, without waiting for your reply to an email. By the time you check your phone, it’s already done.

Three ways you’ll notice this in real life:

- A mandate document setting out your risk profile, restrictions, and objectives

- Ongoing monitoring behind the scenes, you’re not notified of every decision

- Regular performance reports and updates after changes have already been made

The trade-off is clear: you get speed and professional judgment, but you give up individual decision control.

Establishing a Discretionary Mandate

Establishing a discretionary mandate involves a process between the client and manager to define key parameters.

Key Processes:

- Initial Consultation: Clients and managers meet to establish the client’s risk tolerance, financial goals, investment timeframes, and any specific investment restrictions (e.g., ethical or environmental, social, and governance (ESG) preferences).

- Strategy Proposal & Approval: The manager proposes an investment strategy that fits the client’s profile.

- Formal Agreement: The client approves the strategy and signs a discretionary mandate agreement or advisory contract that grants the manager authority to make buy/sell decisions within the agreed limits. This might involve a power of attorney.

- Ongoing Reviews: Annual reviews are conducted with clients to update information and confirm the ongoing suitability of the mandate.

- Autonomous Trading: Within the agreed limits, the manager handles trades autonomously but reports performance to the client (typically quarterly or annually).

Required Documentation:

To ensure compliance and transparency, the following documentation is typically maintained:

- Signed advisory agreements and copies.

- Powers of attorney granting discretion.

- Detailed client profiles (financial situation, objectives, risk assessment).

- Notes from annual reviews and client contact.

- Records of client-requested restrictions.

- Performance reports.

- Suitability updates, usually every 1-2 years.

Typical Client-Requested Clauses/Restrictions:

Clients frequently request certain clauses or restrictions, including:

- Exclusion of specific sectors or companies (e.g., tobacco, alcohol, gambling) or other ethical/ESG exclusions.

- Maximum limits on sector or asset allocation (e.g., no more than 20% in a single stock).

- Specific requirements for tax optimization or income generation.

- Liquidity needs.

- Prohibition from using proprietary funds.

- Avoidance of high-risk assets.

Regulatory Notes:

- Wealth managers must adhere to fiduciary duties.

- All reasonable restrictions imposed by clients must be documented.

- Records are typically maintained for five years or more.

The Real Differences That Change Your Outcome

Control: Who Makes the Final Call

| Service | Who decides |

|---|---|

| Advisory | You, every meaningful change needs your approval |

| Discretionary | Your manager, within the limits you both agreed upfront |

This affects accountability too. With advisory, if you decline a recommendation, that’s your decision. With discretionary, if the manager makes a decision within the mandate that proves poor, they’re accountable. Neither is without risk, they just place risk in different areas.

Speed: How Quickly Changes Can Happen in Volatile Markets

Advisory approval processes are sequential. Advisor contacts you, you read it, you respond, then the trade happens. In a fast-moving market, that chain can take hours or days.

Discretionary managers act within the same working day, sometimes within hours. On a rate cut announcement or a sudden market shock, that difference in timing can matter.

Everyday example: the Bank of England cuts rates unexpectedly at noon. A discretionary manager adjusts bond allocations by 2pm. An advisory client gets an email at 3pm, reads it the next morning, and approves on Thursday.

Time and Effort: How Much of Your Week It Takes

Time expectation:

- Advisory: expect to spend time reading recommendations, asking questions, and replying to approval requests, roughly a few hours per quarter minimum, more during volatile periods.

- Discretionary: mainly periodic review meetings (often quarterly or annually) plus time spent reviewing reports, lighter ongoing involvement.

Monitoring: Periodic Check-Ins vs Constant Oversight

Advisory typically runs on set review cycles, quarterly or annual. Between those meetings, portfolios are usually not being actively watched in most setups.

Discretionary portfolios are monitored continuously. If something moves outside agreed parameters, the manager acts without waiting for a scheduled call.

This matters most in fast-moving markets or if you have a complex portfolio with multiple tax wrappers, pensions, and income needs running in parallel.

Fees in the UK: What You’ll Actually Pay

Typical Fee Structures

| Fee type | Typical range | Common where | What to watch |

|---|---|---|---|

| % of AUM (ongoing) | 0.75%–1.5% pa | Both, used by 81% of advice firms | Compounds over time; check if tiered |

| Fixed annual fee | £1,000–£5,000 pa | Both | £1,500 under £250k; £3,000 for £250k–£500k |

| Hourly rate | £150–£350 | Advisory (ad hoc work) | Hard to predict total cost |

| Initial fee | 2%–3% of amount (advisory); £2,500–£5,000 fixed or % (discretionary) | Both | Sometimes deducted from investment |

| Platform + fund costs | 0.2%–0.45%+ pa | Both | Easy to overlook; adds up significantly |

All-In Cost Examples in Pounds

Here are example all-in costs for different portfolio sizes, including manager fees (at 0.75% for this example), platform fees (at 0.30%), and underlying fund costs (at 0.40%).

| Portfolio Size | Manager Fee (0.75%) | Platform Fee (0.30%) | Fund Costs (0.40%) | Total Annual Cost (£) | Total Annual Cost (%) |

|---|---|---|---|---|---|

| £50,000 | £375 | £150 | £200 | £725 | 1.45% |

| £250,000 | £1,875 | £750 | £1,000 | £3,625 | 1.45% |

| £500,000 | £3,750 | £1,500 | £2,000 | £7,250 | 1.45% |

| £1,000,000 | £7,500 | £3,000 | £4,000 | £14,500 | 1.45% |

This doesn’t sound huge, but over 20 years, the difference between 1.0% and 1.7% all-in costs can take a meaningful chunk out of your final sum through compounding. Always ask for the all-in number in pounds, not just percentages.

When Advisory Can Be Cheaper (and When It Isn’t)

Some advisory models charge lower ongoing percentages, as low as 0.25%–0.75% for ongoing advice in certain setups. If your portfolio is simpler and you don’t need much active management, advisory can cost less.

However, if you need frequent meetings, more administrative time, or your advisor outsources execution to a DFM anyway, those savings narrow fast. Always confirm the full picture before comparing headline numbers.

Investor Protection and Regulation: FCA Rules and FSCS

FCA Regulation: What’s the Same for Both

Both advisory and discretionary services are regulated by the FCA under FSMA. Both require suitability assessments, proper client categorisation, and compliance with conduct rules. Neither is exempt from acting in your best interest, that obligation sits with the regulated firm regardless of the model.

FSCS Protection: What It Does and Doesn’t Cover

FSCS limit: £85,000 per person per firm for eligible investment claims against FCA-authorised firms. This applies if an FCA-authorised firm fails after 1 April 2019.

Your assets are generally held separately from the firm’s own assets and can be transferred. If a firm fails and there’s a shortfall, FSCS covers up to £85,000. Joint accounts qualify per holder.

Eligibility Criteria for FSCS Protection:

- The claimant must be eligible, typically including most private individuals and small businesses.

- The claim must relate to a regulated activity conducted by an authorised firm on or after 28 August 1988.

- The firm must have been declared in default by the FSCS.

- The investment or product must be FSCS-protected (claimants should use the FSCS tool to verify).

Specific Types of Investment Claims Explicitly Excluded from Coverage:

- Unregulated activities or products.

- Claims for failures that occurred before 28 August 1988.

- Non-FCA-authorised investments (e.g., direct shares or equities).

- Business conducted by unauthorised firms.

- Certain mutuals or friendly societies undertaking unregulated activities.

- Claims from financial institutions or collective investment schemes.

- Assets held overseas outside FSCS scope.

Procedure for Invoking FSCS Protection:

Claims for investments typically use the online claims service. Applicants provide supporting documents, such as account statements. The FSCS assesses eligibility and pays out valid claims. This is a free service.

Outsourcing to a DFM: Who’s Still Responsible

Some advisory firms outsource day-to-day portfolio management to a discretionary fund manager (DFM). When this happens, the original firm remains responsible for suitability and the accuracy of the client information passed on.

Practical takeaway: always confirm which FCA-authorised entity makes day-to-day investment decisions, and who is responsible for the advice that resulted in those decisions.

Pros and Cons That Matter Day-to-Day

Discretionary: Upsides vs Downsides

| Pros | Cons |

|---|---|

| No need to approve every trade, genuinely hands-off | Fees are often higher, and all-in costs can reach 2.2% |

| Faster execution during volatile or fast-moving markets | You give up control, individual decisions are made without you |

| Continuous portfolio monitoring, not just quarterly reviews | Performance depends primarily on manager skill and style |

| Access to broader investments and direct market access in many cases | You may not fully understand what’s been done or why until after the fact |

| Particularly useful for complex portfolios with tax planning needs |

Advisory: Upsides vs Downsides

| Pros | Cons |

|---|---|

| Full control, nothing changes without your agreement | Approval delays can mean missed opportunities or slow exits |

| You stay involved and learn how decisions are made | Requires your time and attention, especially in choppy markets |

| Can be cheaper in simpler setups or lower-frequency models | Monitoring is less frequent, things can drift between reviews |

| Useful for building financial confidence over time | Decision stress falls on you when markets are moving and you need to respond fast |

Which One Fits You Best

Discretionary Tends to Fit If You…

- Prefer delegating decisions and staying away from daily market noise

- Are too busy to respond quickly to trade approvals

- Have a higher-value or more complex portfolio, pensions, trusts, ISAs, General Investment Accounts (GIAs) all in play

- Want a manager to act fast during volatility within pre-agreed limits

- Know from experience that you tend to make emotional investing decisions under pressure

Advisory Tends to Fit If You…

- Want the final say on every meaningful portfolio change

- Enjoy being involved and understanding what’s happening with your money

- Have the time to review recommendations and respond without delay

- Feel comfortable holding your nerve during market dips without needing a manager to step in

- Want professional guidance but aren’t ready to hand over full control

Common Scenarios and the Better Default Choice

| Scenario | Better default | Why |

|---|---|---|

| Need rebalancing managed without chasing you for decisions | Discretionary | Manager acts within mandate without needing your input |

| Want to approve every fund switch | Advisory | Approval process built into the service model |

| Expecting big life changes (business sale, inheritance, divorce) | Discretionary | Complex, time-sensitive; needs active management and fast decisions |

| Nervous during market drops and likely to sell at the wrong time | Discretionary | Manager holds the line within agreed risk limits |

| Confident investor wanting a second opinion | Advisory | Guidance without handing over control |

| Portfolio across ISAs, pensions, GIAs with active tax planning | Discretionary | Multi-wrapper complexity suits ongoing active oversight |

Questions to Ask Before Signing Anything

- Who makes trades day-to-day, and what specifically requires my approval?

- Can I see the mandate or risk limits in writing, and what would trigger a review of those limits?

- What is the all-in annual cost including platform and fund costs, give it to me in pounds and percentage?

- How often is my portfolio monitored, and what happens between formal reviews?

- How is performance measured, against what benchmark, and how often is it reported to me?

- What happens if I disagree with a recommendation (advisory) or want to exclude certain holdings (discretionary)?

- Can you confirm your FCA authorisation details and walk me through the complaint process and FSCS eligibility?

- Do you use in-house funds or model portfolios, and do you receive any referral fees I should know about?

Mini Glossary

Discretionary mandate: written authority given to a manager to buy and sell within agreed limits without client approval each time.

Advisory mandate: an arrangement where the advisor recommends but the client retains final decision-making authority over all portfolio changes.

Suitability: the regulatory requirement that any recommendation or investment decision must be appropriate for your personal circumstances, goals, and risk tolerance.

Risk profile: a formal assessment of how much investment risk you’re willing and able to take, used to define the boundaries of a discretionary mandate or frame advisory recommendations.

AUM fee: a fee charged as a percentage of the total value of assets under management; the most common charging method in the UK.

Platform fee: a separate charge levied by the investment platform (the technology and custody layer) on top of the manager’s fee.

Benchmark: a reference index or target used to measure investment performance. The MSCI WMA Private Investor Indices are standard benchmarks for UK wealth management.

DFM (Discretionary Fund Manager): a firm or team with delegated authority to manage investments on a discretionary basis; sometimes used by advisory firms who outsource portfolio management.

Conclusion: Pick Based on Control, Speed, and Total Cost

- Match the service to how involved you realistically want to be, not how involved you think you should be.

- Compare all-in fees, not just the headline management charge, platform and fund costs can add 0.5%–0.8% before you’ve seen a single trade.

- Choose the setup you can actually stick with through a bad market year, because that’s when the wrong choice will cost you most.

FAQs

What does discretionary mean in wealth management?

Discretionary means your investment manager has authority to make trades and portfolio changes on your behalf without needing your approval each time. You agree the strategy and risk boundaries upfront, the mandate, and the manager works within those limits. You stay informed through regular reports, but you’re not in the decision loop day-to-day.

What is the difference between DPMS and NDPMS?

DPMS stands for Discretionary Portfolio Management Service, the manager makes decisions within agreed parameters without client sign-off on each trade. NDPMS stands for Non-Discretionary Portfolio Management Service, which is effectively the advisory model, the manager recommends, but the client must approve before anything is executed. The core difference is where decision authority sits.

Is a 1% fee for a financial advisor worth it?

It depends entirely on what you’re getting for it and what your total all-in cost actually is. A 1% AUM fee sounds straightforward, but once you add platform costs (0.2%–0.45%) and underlying fund charges (0.3%–0.5%+), you can be at 1.5%–2% all-in. If the service includes active tax planning, pension management, and continuous oversight, that cost may well be justified. If it’s a model portfolio with a quarterly call, it’s worth questioning. Always ask for the all-in figure in pounds, then judge whether what you’re getting is worth that number.

What is the difference between discretionary and non-discretionary wealth management?

These are two names for the same distinction covered throughout this article. Discretionary management means the manager acts within agreed limits without asking you first. Non-discretionary management (advisory) means the manager advises but you retain control, nothing changes without your say-so. The choice comes down to how much control you want, how quickly you need decisions made, and whether you have the time and knowledge to stay actively involved.