Wealth vs. Prosperity: How to Build a Life of True Abundance

Most people think earning more will fix the feeling. It doesn’t. You get the raise, upgrade the apartment, and three months later you’re back to that same low-grade anxiety, just with higher monthly payments. The problem isn’t your income. It’s that you’re optimizing for one thing while neglecting everything else.

Here’s a solution: separate wealth (your net worth – what you own minus what you owe) from prosperity (actually living well – money, health, relationships, time, and peace of mind working together). When you stop treating net worth as the only scoreboard, you can build a money plan that supports the parts of life that actually matter.

Wealth vs. Prosperity: Clear Definitions and the Real Difference

Wealth

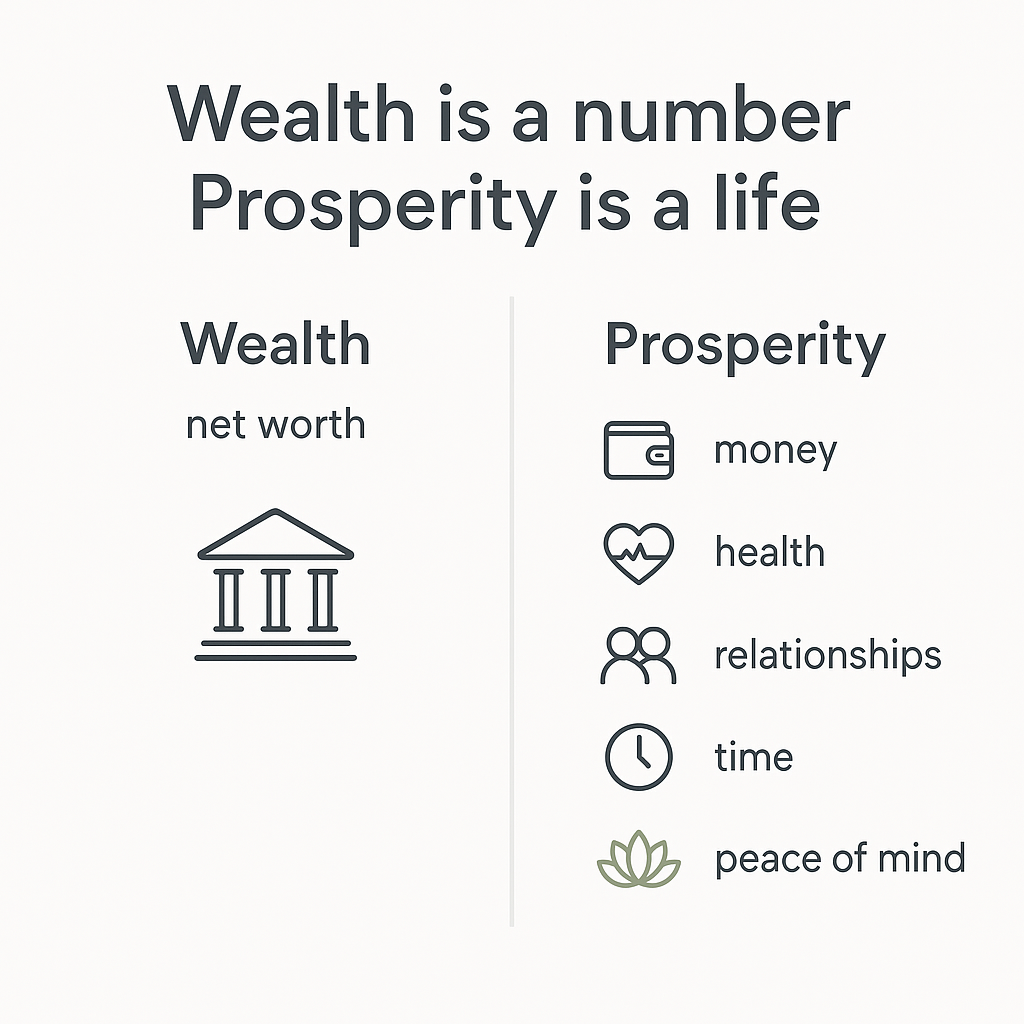

Wealth is simple math. Wealth = what you own minus what you owe = net worth. It’s a number on a spreadsheet. It tells you how much financial buffer you have, not how your life feels on a Tuesday morning.

Prosperity

Prosperity is bigger. Prosperity = living well overall – enough money + health + strong relationships + time + peace of mind + purpose. It’s not anti-money. It’s the full picture that money alone can’t complete.

The Difference in One Line

Wealth is a number. Prosperity is a life.

Wealth vs. Prosperity at a Glance

| Wealth | Prosperity | |

|---|---|---|

| How it’s measured | Net worth (assets minus liabilities) | Day-to-day life quality |

| What it’s for | Options and financial security | Well-being and meaning |

| What can break it | Bad debt, low or no income | Burnout, loneliness, poor health |

| What it looks like | Assets, investments, savings | Calm mornings, healthy body, people you trust |

| The trap | More never feels like enough | Neglecting finances and calling it “simple living” |

How Day-to-Day Life Quality is Measured for Prosperity

Measuring day-to-day life quality involves assessing several dimensions of well-being, beyond mere financial indicators. Some frameworks for this include:

-

Health-Related Quality of Life (HRQOL) Metrics (CDC HRQOL-4):

- Self-rated general health: A 5-point scale (1=excellent to 5=poor).

- Days of poor physical health: Over the past 30 days.

- Days of poor mental health: Over the past 30 days.

- Days of activity limitations: Over the past 30 days.

-

Quantified Quality of Life Measures:

- Quality of Life Index (QLI): Scores from 0-10 across physical, psychological, and social functioning.

- SF-36: Measures physical and mental health across 8 domains.

- WHOQOL-BREF: Uses varying 5-point response scales.

These metrics offer a way to understand the tangible and subjective experiences that contribute to a person’s overall quality of life, which is central to prosperity.

Quick Net Worth Example

Net Worth = Assets − Liabilities

- Assets: $520,000 (home equity, retirement account, savings, car)

- Liabilities: $350,000 (mortgage, student loans, car loan)

- Net Worth: $170,000

That $170K is your wealth. Whether life feels good? That’s a separate question.

Wealth – What It Is, How It’s Built, What It’s Actually Good For

Assets vs. Liabilities – Kept Simple

Assets put value on your side of the ledger:

- Cash (savings and checking accounts)

- Retirement accounts (401k, IRA)

- Stocks and bonds

- Real estate (home, rental property)

- Business equity

Liabilities pull value away:

- Mortgage

- Student loans

- Credit card balances

- Car loans

- Personal loans

The gap between those two columns is your net worth.

What Wealth Is Great At – and What It Can’t Do

Wealth does some things really well:

- Provides stability when income dips

- Creates options (you can leave bad jobs, bad situations)

- Handles emergencies without spiraling into debt

- Gives you negotiating power at work

- Lets you support family members or causes you care about

But here’s the blunt limit: money reduces certain kinds of stress. It does not automatically fix relationships, physical health, or how you see yourself. Plenty of high earners are anxious, isolated, and running on empty. The bank account is fine. Everything else isn’t.

Prosperity – What It Looks Like in Real Life

The Prosperity Stack

Prosperity has five pillars. None of them are complicated. All of them require attention.

- Body: You have energy. You sleep. You move consistently.

- Mind: Anxiety isn’t running the day. You have some steadiness.

- People: You have close relationships and at least some sense of community.

- Time: You have breathing room. Not every day is a sprint.

- Meaning: There’s something worth doing, even on hard weeks.

Miss one pillar for long enough and the others start to crack.

Actionable Methods for Mind Steadiness

Developing steadiness of mind and reducing anxiety involves consistent practice of psychological techniques. Here are concrete steps and examples:

-

5-4-3-2-1 Grounding:

- Steps: Name 5 things you see, 4 things you can touch, 3 things you hear, 2 things you smell, and 1 thing you taste.

- Purpose: To anchor yourself in the present moment when anxiety spikes.

-

Box Breathing:

- Steps: Inhale through your nose for 4 seconds, hold for 4 seconds, exhale through your mouth for 4 seconds, and hold for 4 seconds. Repeat at least 4 times.

- Purpose: To regulate the nervous system and calm the mind.

-

Breath Focus:

- Steps: Inhale through your nose for 3 seconds, exhale through your mouth for 3 seconds. Focus solely on the sensation of each breath for 3 minutes.

- Purpose: To improve concentration and reduce mental chatter.

-

Calm Core Breathing:

- Steps: Inhale through your nose for 4 seconds, exhale through your mouth for 8 seconds. Visualize your mind as a settling pond for 2-3 minutes.

- Purpose: To deepen relaxation and mental clarity.

-

Mindful Body Scan:

- Steps: Close your eyes, inhale and exhale intentionally. Systematically scan your body from head to toe (or vice versa), noticing any areas of tension. Release tension on the exhale.

- Purpose: To increase body awareness and relieve physical manifestations of stress.

-

Watch Thoughts Float:

- Steps: Focus on your breath for 2 minutes. When a distracting thought arises, visualize placing it on a leaf or cloud and watching it float away without judgment.

- Purpose: To develop detachment from anxious thoughts.

Practice these techniques daily for 5-10 minutes, and use them when anxiety arises.

Signs of Prosperity You Can Feel This Week

| Sign | What it looks like |

|---|---|

| Waking up without dread | You’re not immediately stressed before the day starts |

| Fewer money arguments | Finances aren’t a constant source of conflict |

| Consistent routines | Sleep, movement, meals aren’t chaotic |

| Saying “no” without panic | You have enough margin to decline |

| One person to call | Someone picks up when it’s hard |

These aren’t luxuries. They’re signals that the life structure is working.

Wealth Without Prosperity vs. Prosperity Without Great Wealth

Wealth Without Prosperity – How It Shows Up

Research is clear on this: tying your self-worth to financial success increases stress, drives negative social comparisons, and fuels anxiety, even when you control for how much money someone actually has. High financial-contingent self-worth is linked to more disengagement, more negative emotion, and less sense of autonomy when money stress hits.

In real terms, it looks like this:

- High earner, no time: Making $300K, working 70-hour weeks, barely sees their kids, can’t remember the last vacation that didn’t include Slack.

- Savings anxiety: Has $80K in the bank, still loses sleep over money, constantly checks the account, always feels behind.

- Status spending: Buys things to signal success, racks up credit card debt, net worth is actually negative beneath the surface.

The hedonic treadmill is real. You hit a goal, adapt, and the bar moves. More feels necessary. It rarely satisfies.

Prosperity Without Great Wealth – Real Examples

Research from Germany captured this well:

Jürgen Hellmuth runs a bakery in a small Hessian town. He has 26 staff, works long days, and genuinely enjoys the work. He built customer loyalty through craftsmanship and treating his staff well, not by competing on price. The nearby supermarket sells pretzels for €0.30. He doesn’t race them to the bottom.

Marianus and Aaron (Restaurant Klinker) made a deliberate choice to prioritize happiness and wellbeing over profit maximization. They define prosperity as quality of life, not financial accumulation.

One unnamed woman stepped down from managing a large company to run a small store. Her own words: “Thank goodness… I can keep it balanced just in a way I like because it’s much smaller business. I control it much easier. It’s much less pressure and much less stress.”

None of these people are wealthy by conventional metrics. All of them are prospering.

The Trade-Offs People Miss When Chasing Wealth

Costs That Don’t Show on a Bank Statement

- Hedonic treadmill: Every new income level becomes the new normal. The relief is temporary.

- Time squeeze: Long hours erode relationships slowly. You don’t notice until the drift is wide.

- Health trade: Chronic stress, poor sleep, and burnout have real physical costs that money eventually has to fix, if it can.

Strategies to Prioritize Time Over Money

Consciously prioritizing time over money, especially when faced with financial pressures, requires specific strategies:

- Pay Yourself First with Time: Block out time for your priorities (e.g., skill development, exercise, family) before scheduling anything else. Schedule these during high-energy periods.

- Invest Time Like Money (ROI): Evaluate activities based on their return on investment (future value, savings, happiness). Prioritize high-return tasks (e.g., deep work) over low-return ones.

- Prioritize Needs vs. Wants Daily: Create a morning to-do list, distinguishing between “Needs” (time-sensitive, essential) and “Wants” (important but flexible). Plan days and anticipate big tasks.

- Outsource Disliked Tasks: Consider paying for chores (e.g., laundry, cleaning) to free up your time. The well-being gained can outweigh the monetary cost, especially under financial pressure.

- Delegate and Say No: Assign tasks to others with deadlines. Consult trusted individuals before committing to new time obligations. Decline low-value opportunities.

- Calculate “Happiness Dollars”: Recognize that experiences like vacations, socializing, and active leisure often provide greater well-being than short-term monetary gains. Remind yourself that time can be more valuable than money for overall happiness.

- Eliminate Waste: Audit your time sinks (e.g., excessive scrolling, unproductive deal-hunting). Maximize high-value activities and organize your environment to reduce interruptions.

Two Research Anchors Worth Knowing

A study of N=4,690 participants found that valuing time over money was consistently linked to higher subjective well-being. The trade-off between them is real, and most people default to optimizing for money.

On income and happiness: the often-cited idea is that happiness plateaus around $100K annually for people who are already unhappy. But newer research suggests that for many people, especially those who are already reasonably content, income gains continue to improve well-being beyond that. The key nuance: income helps, but non-financial factors (relationships, meaning, health) remain essential regardless of income level. More money doesn’t make those irrelevant.

When the Wealth Push Makes Sense

Some seasons of life call for aggressive wealth-building. Those include:

- Escaping high-interest debt

- Building a safety net for the first time

- Supporting dependents, kids, aging parents

- Funding a specific health need

In those cases, the trade-offs are worth it. But they should be temporary and deliberate, not the permanent default.

Build Wealth That Serves Prosperity: A Simple Life-Plan

This is the part that actually matters. Here’s how to make money serve life, not the other way around.

1. Define your “enough” number

Add up your basic monthly costs, a safety margin, and one or two life priorities. That’s your target.

Example: $3,200 (rent, food, bills) + $500 (buffer) + $300 (one priority – gym + occasional travel) = $4,000/month as “enough” right now.

Without a number, you’ll always feel like you need more.

2. Track net worth monthly – not daily

Pick one app or one spreadsheet. Set one date per month to update it. List your assets. List your debts. Calculate the gap. That’s it. Daily checking is anxiety, not strategy. For tools, tips, and templates to make this process painless, check resources like Get Rich Slowly.

3. Build a boring safety net first

Start with one month of expenses saved. Then build to three months. Before investing aggressively, kill high-interest debt. The math is simple: paying 20% interest on a credit card while earning 7% in an index fund is a net loss. For practical, step-by-step guides on building emergency funds and sensible saving plans, see Get Rich Slowly.

Calculating Safety Nets (1 or 3 Months of Expenses)

To calculate a safety net of expenses, you need to determine your actual essential monthly spending. This calculation focuses on “needs” rather than “wants.”

Steps to Calculate:

- Track Actual Spending: Review bank and credit card statements for the last 3-6 months. Categorize every transaction. Avoid estimating; use real data.

- Identify Essential Expenses (Needs):

- Housing: Mortgage/rent, property taxes, condo fees, homeowners’ insurance, escrow accounts.

- Utilities: Electricity, gas, water, sewage, internet, phone.

- Transportation: Car payments/leases, gas, insurance, public transit, parking, maintenance tools.

- Food: Groceries and essential home meals (exclude dining out that isn’t a necessity).

- Insurance: Health, auto, homeowners.

- Debt Payments (Minimums): Credit card, car loan, student loan, personal loan.

- Other Necessities: Daycare, medications, work-related uniforms.

- Exclude Discretionary Spending (Wants): Do not include things like entertainment, luxury dining, vacations, subscriptions you don’t need, or non-essential shopping. These can be cut during an emergency.

- Calculate Average Monthly Essential Expenses: Sum up your essential spending for the tracking period and divide by the number of months.

- Determine Safety Net Goal:

- One Month Goal: Multiply your average monthly essential expenses by 1.

- Three Month Goal: Multiply your average monthly essential expenses by 3.

Example Calculation:

If your average essential monthly expenses are $3,000:

- One Month Safety Net: $3,000 x 1 = $3,000

- Three Month Safety Net: $3,000 x 3 = $9,000

Common Pitfalls to Avoid:

- Estimating instead of tracking: Always use actual financial records.

- Forgetting irregular expenses: Account for annual costs (e.g., car registration, insurance premiums paid annually) by dividing them by 12 and adding to your monthly average.

- Using gross pay: Base calculations on your net (take-home) pay.

- Including wants: Strictly differentiate between needs and wants when calculating an emergency fund.

4. Automate the basics

Willpower is not a system. Set up auto-transfers to savings the day after payday. Autopay your bills. Calendar a monthly money check-in. When the right action happens automatically, you stop fighting yourself.

5. Buy time before you buy status

One hour of time saved per week compounds. Pay for meal prep, a monthly cleaner, or a commute that doesn’t destroy you, before you upgrade the car or the watch. Time directly reduces daily stress. Status rarely does.

6. Filter your spending with three questions

Before a non-essential purchase:

- “Does this solve a real problem?”

- “Will I still care about this in 3 months?”

- “Does this create a new monthly payment?”

If the answer is no, no, and yes, skip it.

7. Use money as a tool – not a scoreboard

Direct money toward things that reflect what you actually value: supporting family, giving, ethical earning, building something. The Stoics had it right: wealth is useful, but character runs the show. Seneca put it plainly: enjoy what you have without clinging to it, and use it well.

Quick Self-Check: Are You Building Wealth, Prosperity, or Both?

10-Minute Wealth vs. Prosperity Check

| Area | This is strong | This needs work |

|---|---|---|

| Net worth trend | Consistently moving up | Flat or declining |

| Debt stress | Low, manageable | Constant, overwhelming |

| Sleep consistency | 7+ hours, regular schedule | Irregular, poor quality |

| Exercise/movement | 3+ times per week | Rarely or never |

| Quality time with key people | Weekly, intentional | Weeks pass without it |

| Time freedom | Some unscheduled hours weekly | Every hour is accounted for |

| Work meaning | Mostly purposeful | Feels pointless most days |

| Daily anxiety | Low baseline | High, hard to switch off |

| Savings rate | Consistent monthly contributions | Irregular or none |

| Surprise bill readiness | Could handle $1,000 without panic | Would cause serious stress |

Run this check once a month. More than four “needs work” answers means the plan needs adjusting, either the money side or the life side.

Stoicism – Only the Parts That Are Actually Useful

Wealth as “Helpful, Not Holy”

The Stoics called wealth a “preferred indifferent.” It’s nice to have. It’s useful. But it’s not required to live well, and it’s not going to make you a good person by default. Seneca said it clearly: enjoy what you have without clinging to it, and use it in ways that don’t harm others. That’s the whole framework.

Pursuing wealth obsessively, making it the point, historically leads to what the Stoics warned about: greed, anxiety, and a life spent chasing an external thing that can always be taken away.

Specific Stoic Techniques for Financial Anxiety

Beyond general principles, Stoicism offers practices to manage anxiety, especially during financial uncertainty:

- Mindful Spending & Temperance: Practice pausing before purchases. Distinguish between needs and wants. View money and possessions as transient and non-essential for happiness.

- Premeditation of Adversity (Premeditatio Malorum): Mentally prepare for potential financial setbacks like job loss or market downturns. By considering these possibilities, you reduce their emotional impact if they occur, freeing up energy from worry.

- Focus on the Controllable: Concentrate your efforts on what you can influence: your spending habits, your skills, your saving rate. Let go of worry over external market fluctuations or global events.

- Cultivate Gratitude: Daily reflect on what you already possess (a job, shelter, basic needs met) to counter the feeling of lack and reduce anxiety.

- Nighttime Release Ritual: If financial anxiety arises before sleep, acknowledge the worry. Remind yourself that ultimate outcomes are not entirely within your control. Release these worries through reflection or journaling, effectively “putting them down” for the night.

- Pause and Freeze Moment: In moments of financial stress or market volatility, stop. Notice your physiological response (rapid heart rate, shallow breath). Then, calmly decide on an intentional response rather than reacting impulsively.

Control What You Can, Let Go of the Rest

You control your habits, your choices, your character. You don’t control markets, luck, or what other people think of your financial decisions. Confusing the two is a reliable path to chronic stress.

Minimalism – Needing Less, Not Owning Nothing

Minimalism isn’t about living in an empty room. It’s about reducing wants to reduce pressure. Fewer unnecessary expenses means less financial stress without sacrificing joy. Cutting a subscription you don’t use isn’t sacrifice, it’s clarity.

Common Questions

Is prosperity just another word for being rich?

No. Prosperity includes financial stability, but it also covers health, relationships, time, and purpose. You can be rich and not prosperous. You can be prosperous without being rich.

Can you be prosperous with debt?

Yes, if the debt is manageable, low-interest, and not causing constant stress. High-interest debt that dominates your mental bandwidth actively undermines prosperity. The goal is debt that doesn’t run your life.

How much money do you need to feel secure?

It depends on your housing costs, dependents, health situation, and location. A practical anchor: cover your basics, maintain a cash buffer, and keep a consistent savings rate. The specific number varies, the structure matters more than the figure.

What if I want both a meaningful life and a lot of money?

That’s a legitimate goal. The key is sequencing and intention. Build the financial side in a way that doesn’t destroy the other pillars while you’re doing it. It’s possible, but it requires being honest about the trade-offs you’re making and which ones are temporary versus permanent.

What’s one change that helps fast?

Track your spending for 7 days, every transaction. Then reclaim one block of time per week that currently goes to something low-value. Those two moves together show you where your money and time are actually going, which is the prerequisite for changing either.

Which corner attracts money?

This comes from Feng Shui, which points to the southeast corner of a home as associated with wealth and abundance. Whether you believe in it or not, the underlying idea, intentionality about your environment and where you focus attention, is consistent with building better money habits.

What is the difference between prosperity and accumulation of wealth?

Wealth accumulation is adding to your net worth, assets minus liabilities. Prosperity is the overall quality of your life. You can accumulate wealth without prospering, and you can prosper without accumulating significant wealth. They overlap but are not the same thing.

What’s the difference between wealth and being rich?

“Rich” is relative, it usually means having a high income or appearing affluent. “Wealth” is structural, it’s your net worth, the actual gap between what you own and what you owe. A high earner with no savings and significant debt is rich by appearance, not wealthy by definition.

What’s the difference between fortune and prosperity?

Fortune typically refers to accumulated money or assets, luck or circumstance included. Prosperity is broader and more deliberate: it includes financial stability but also health, relationships, and purpose. Fortune can be inherited or stumbled into. Prosperity is generally built.

Closing

Build wealth for safety and options. Build prosperity for a life you actually enjoy. And make sure your money plan supports your relationships, your health, and your time, not just your net worth number.

One concrete next step: pick one item from the life-plan above and do it this week. Not all seven. One.